Representative End User Clients

Representative Automation Clients

Representative Software Clients

A company incurs capital expenditure (CapEx) to acquire or upgrade physical assets, including property, plant, and equipment. In this periodic report, ARC Advisory Group looks at a number of different manufacturing industries to identify the current CapEx trends in India. We calculate CapEx in two separate segments: based on the money spent on acquiring and upgrading total fixed assets, and on the money spent on acquiring and upgrading the plant and machinery.

While ARC also publishes a separate global Capital Expenditures report for leading industries in all world regions, this report focuses exclusively on India’s capital expenditure analysis and includes the CapEx trends for leading industries in the country. These include automotive, cement, chemical & petrochemical, electric power, metals, oil & gas and refining, food & beverage, and pharmaceutical.

Industrial companies are seizing the present growth opportunities that India offers. Companies are building best-in-class industrial facilities to meet the growing needs of the country’s expanding consumer class. Major investments have been planned for infrastructure development. These should help push the domestic steel companies to increase production. The plan to expand and upgrade refineries to meet India’s Bharat Stage (BS) emissions standards for vehicle fuels has also been implemented.

The Government of India implemented BS VI transportation fuel mandate on April 1, 2020. Despite many challenges, India successfully managed timely implementation of BS VI. This new emission standard required significant changes in hardware, like improvements in engine combustion, calibration along with the introduction of after-treatment devices; and all this required heavy investments. However, with the collaborative and focused approach across the value chain, India ensured the smooth transition.

While sectors like power generation and cement are currently burdened with overcapacity and underutilization of assets, eventually, the rise in domestic demand should increase value creation through these assets. On the infrastructure front, the government has allocated huge investments for building roads, railways, airports, and ports; and companies are likely to ramp up their capacity expansion activities to meet domestic demand in the coming years. According to ARC Advisory Group’s India CapEx Survey, capital spending as a percentage of revenue has decreased for all the industries due to the impact of COVID-19.

With the decline in overall CapEx, 2020 was the worst year for all the industries in India. During the COVID-19 pandemic, lockdowns and factory shutdowns resulted in cessation of economic activity. The manufacturing output decreased, which reflected a fall in the external as well as domestic demand.

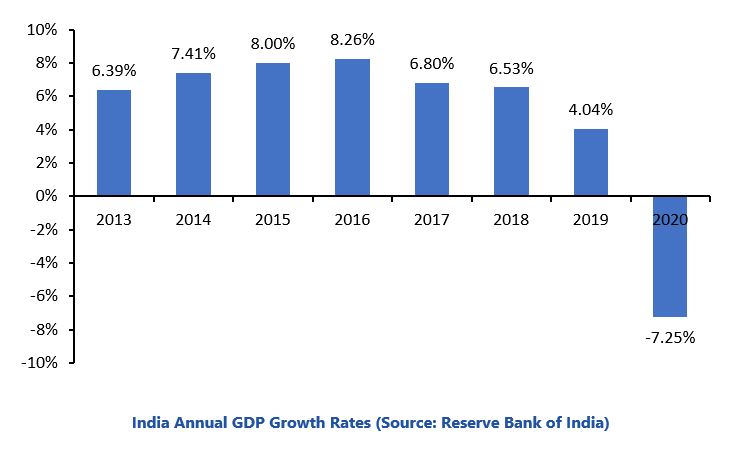

India’s GDP was approximately $2.62 trillion with a per capita GDP (PPP) of around $6,454 in 2020. India’s GDP value fell to -8.6 percent in 2020 when compared with 2019. In terms of purchasing power parity, India’s GDP, was valued at around $8.7 trillion, and it was the third largest in the world in FY 2020-21.

According to the provisional National Income estimates, the country’s GDP contracted by 7.3 percent in FY 2020-21, compared with 4.0 percent in FY 2019-20. The IMF has projected a growth of 9.5 percent for the Indian economy in 2021. The economy is reviving from the contraction from the last fiscal year, as well as the second wave of COVID-19 faced in March-May 2021. The country’s GDP is mainly driven by the service sector, which constitutes over 55 percent, including information technology (IT) and IT-enabled services (ITES). Agriculture is the main occupation in India, and the Gross Value Added by agriculture, forestry, and fishing was estimated at $276.37 billion in FY2020-21.

The Purchasing Manager’s Index (PMI) for the manufacturing sector, improved in September 2021 as companies benefitted from strengthening demand conditions amid the easing COVID-19 restrictions. India’s PMI improved from 52.3 in August 2021 to 53.7 in September 2021, indicating a stronger expansion in overall business conditions across the manufacturing sector.

National Manufacturing Policy aims to uplift the manufacturing sector and has set a target of 25 percent share of GDP from manufacturing by 2022. The government plans to infuse $26 billion investment in the manufacturing sector, over the next five years, starting FY 2021-22. The country’s overall exports (merchandise and services combined) aggregated at around $493.2 billion in April-March 2020-21, exhibiting a negative growth of -6.66 percent over the same period last year. Cumulative value of exports for the period April-March 2020-21 was $290.6 billion as against $313.4 billion during the same period in 2019-20, registering a negative growth of -7.3 percent. India’s cumulative value of imports for the period April-March 2020-21 was $389.2 billion, as against $474.7 billion during the same period in 2019-20, registering a negative growth of -18.02 percent. Major industries in India include textiles, telecommunications, chemicals, food & beverage, steel, cement, refining, electric power, pharmaceuticals, and IT & software.

ARC Advisory Group’s India Capital Expenditure Survey 2020 tracks total capital expenditure, capital expenditure on plant and machinery, total revenue, total assets, and asset turnover. The sample size includes 88 companies from eight major industries representing more than $380 billion revenues in 2020. This capital expenditure survey is based on the analysis of the information from the annual reports of India’s leading companies in the following key growth industries: automotive, cement, chemical & petrochemical, electric power, metals, oil & gas, and refining, pharmaceutical, and food & beverage.

Consumption has been the major contributor to India’s growth story. However, consumption expenditure decelerated due to the pandemic. Private Final Consumption Expenditure (PFCE) contracted by 9.0 percent in 2020-21, reflecting cliff effects of the impact of the stringent nationwide lockdown and social distancing norms. The consumption levels declined in both rural and urban areas. Although both rural and urban areas faced a severe impact, contraction in private consumption has been more pronounced in case of the latter.

In recent years, the economy witnessed a gradual transition from a period of high and variable inflation to more stable, low-level inflation through 2018. The inflation rate had been decreasing gradually from 12.3 percent in 2008 to 3.6 percent in 2018. However, the inflation rate increased to 6.2 percent in 2020 due to factors, such as supply side inflation and increased labor cost, which increased commodity prices.

The declining exchange rate for the rupee is affecting the country’s economy, making imports more expensive. However, some imports, such as oil, cannot be reduced, negatively impacting the country’s deficit. The rupee is expected to depreciate further over concerns about the US-China trade war, a slowdown in global trade, foreign institutional investment (FII) outflow pressures, and the political uncertainty.

National Manufacturing Policy aims to uplift the manufacturing sector and has set a target of 25 percent share of GDP from manufacturing by 2022. The government plans to infuse $26 billion investment in the manufacturing sector, over the next five years, starting FY 2021-22. The policy also aims to enhance the manufacturing sector’s global competitiveness. Some of the related initiatives include setting up a national manufacturing and investment zone (NMIZ) to promote investments in the manufacturing sector, green technologies, and skill development programs to cater to the needs of the manufacturing sector. The policy should enable the country to emerge as a global manufacturing hub with extended forward and backward integration with the global supply chain.

While the state can only create the necessary policy ambience, the key players who can exploit the growth opportunities are the industry thought leaders. Meeting the consumer demand, which continues to remain relatively good compared with many other countries, rests with the industrial companies and the strategies they adopt to fulfill the demand while protecting their margins. While there is further scope to refine it, the state has played its part by announcing the NMP.

India’s economic growth continues to propel demand for fuel, energy, and basic materials. CapEx as a percentage of revenue declined for every industry; however, electric power’s CapEx was higher compared to other industries. NTPC, Neyveli Lignite, and Power Grid Corporation of India Ltd. (PGCIL) share the majority of the capital investments for generation and transmission, respectively. The oil & gas and refining and electric power industries are major investors in capital assets and made significant capital investments in 2020.

Two wheelers and passenger vehicles dominate the domestic Indian auto market. Small and mid-sized cars, in turn, dominate passenger car sales. Two wheelers and passenger cars accounted for 80.8 percent and 12.9 percent market share, respectively, accounting for a combined sale of over 20.1 million vehicles in FY20. Overall, automobile exports reached 4.8 million vehicles in FY20, growing at a CAGR of 6.9 percent during 2016-20. Two wheelers made up 73.9 percent of the vehicles exported, followed by passenger vehicles at 14.2 percent, three wheelers at 10.5 percent, and commercial vehicles at 1.3 percent.

Auto makers in India produce the entire range of passenger vehicles: multi-utility vehicles (MUVs), sports utility vehicles (SUVs), commercial vehicles, trucks, buses, tractors including farm, earthmoving, and construction equipment, and two- and three-wheelers. The country is becoming a global hub for automotive manufacturing, with increasing presence of the world’s top auto majors.

2020 had a rough beginning with lack of consumer spending, more private investments, weak monsoon season, and the automotive sector was on a weak footing with the imposition of BS-VI norms. Moreover, the COVID-19 lockdown worsened the situation, leading to a severe drop in the manufacturing and selling statistics. Slow economic activity, increased cost of vehicle ownership, a drop in the purchasing power, high GST rates, stagnant wages, and liquidity concerns all affected automotive sales in India.

Production cuts by automakers have resulted in job losses in vehicle manufacturing, component making, and vehicle distribution industries. The automotive sector contributes around 49 percent to the manufacturing GDP and employs approximately 37 million people. Due to COVID-19 the Indian automotive industry suffered Rs. 2,300 crore loss per day and as per a parliamentary panel report, “an estimated job loss in the sector was about 3.45 lakh.”

Considering the crisis, the industry is likely to go through at least two consecutive years of severe contraction, leading to low level of capacity utilization, lack of future CapEx investment, high risk of bankruptcy and job losses across the entire automotive value chain. With the current COVID-19 pandemic the rate of job loss is expected to increase during the next few years. Many automotive manufacturers are reducing their production and dealerships to reduce expenses and compensate for the low rate of sales. Given the present situation, the government must consider lowering GST rates on automobiles to trigger sales.

Capital spending in the automotive industry is around 1 percent of revenue. Out of the total CapEx, the automotive industry spends over 40 percent on plants and machinery. The overall revenue has been increasing since 2015 until 2018. The market started witnessing a dip in sales from 2019 onwards, and in 2020 also there was dip in sales. The sales-per-asset remained more-or-less stagnant until 2018. The automotive industry witnessed one of the slowest years in 2020 due to lack of consumer spending, more private investments, weak monsoon season, and the imposition of BS-VI norms.

As per the data of the Society of Indian Automobile Manufacturers (SIAM), during the financial year 2019-20, the Indian auto sector witnessed a drop of around 18 percent in domestic sales. In addition to the above issues, COVID-19 also impacted the automotive market’s manufacturing and selling statistics. COVID-19 has changed market dynamics and buying patterns. With priority on safety and social distancing, consumers prefer to avoid visiting a showroom to buy a vehicle; and that has led to the rapid adoption of digitalization and contactless vehicle buying experience.

India’s cement industry is expected to increase its total installed capacity to about 550-600 million tons per annum (MTPA) by the year 2025. India, the second largest cement producer in the world, accounted for over 7 percent of the global installed capacity as of 2020. With around 210 large cement plants and 350 small cement plants, India’s cement industry has tremendous potential for future growth due to the robust growth in housing, infrastructure & construction, and other sectors. The escalating demand for housing and office complexes, hotels, hospitals, roads and highways, multiplexes, industrial construction, and so on spurs the growth of the cement industry in India. Cement production reached 329 million tonnes (MT) in FY20. The cement production capacity is estimated to reach 381 MT by FY22. Of the total capacity, 98 percent lies with the private sector and the rest with the public sector. The top 20 companies account for around 70 percent of India’s total cement production.

Growth in infrastructure and real estate sector, post-COVID-19 pandemic, is likely to augment the demand for cement in 2021. The industry is likely to add approximately 8 MTPA capacity in cement production. Global companies entered the Indian market in the last decade lured by the opportunities in this industry. Some also plan to add production capacities through new projects or brownfield project expansions.

According to the ARC India CapEx Index, capital spending in the cement industry is around 0.4 percent of revenue. Out of this total CapEx, the industry spends over 60 percent on plants and machinery. Growth declined in 2020 majorly due to spread of COVID-19. The subdued demand from the real estate market, rising prices of raw materials, and allegations of cartelization for deliberate price hike plagued the industry in the year 2020. The observed decline in the CapEx/revenue trend was due largely to the decline in CapEx of most of the major cement manufacturers.

ARC Advisory Group clients can view the complete report at ARC Client Portal

If you would like to buy this report or obtain information about how to become a client, please Contact Us