Representative End User Clients

Representative Automation Clients

Representative Software Clients

A global upswing started in 2017, and the momentum continued in 2018. However, 2019 marked a turning point in the business cycle for many discrete manufacturing industries with 2020 and maybe 2021 expected to experience a slowdown. This report tracks the recent developments and trends of the discrete manufacturing industries and provides a five-year forecast.

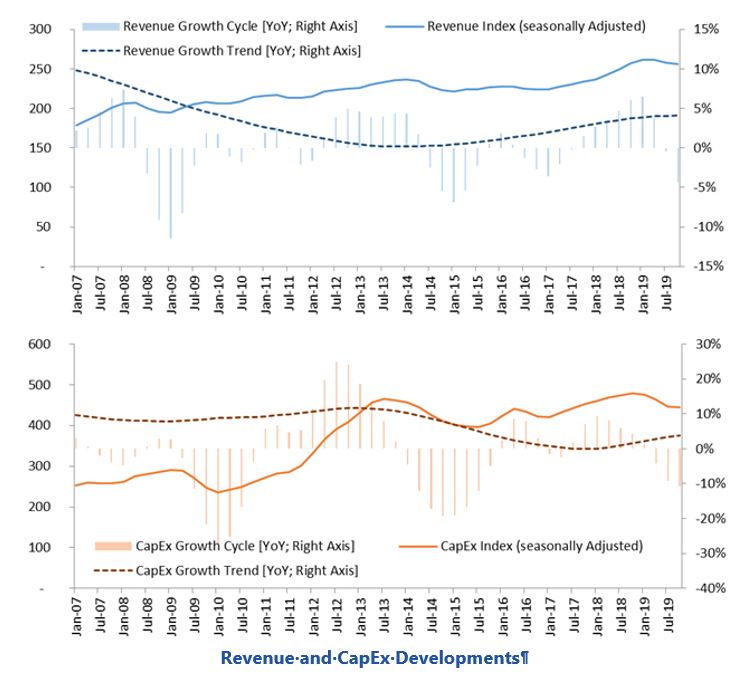

ARC Advisory Group looks at different discrete manufacturing industries to identify trends in capital expenditures (CapEx) and their drivers. We calculate our CapEx index using the same rigorous methodology we use for the ARC Automation Index, which is based on publicly available data provided by major companies (end users rather than suppliers in this case).

Capital expenditures (CapEx) are a leading indicator for automation markets. When confidence in vertical industry markets decline, a decline in investments often follows.

There are a number of headwinds that are stalling investment in the discrete manufacturing industries, firstly political uncertainty and the ongoing trade tensions e.g. US-China trade war, Brexit, etc. The emergence of the novel coronavirus (COVID-19) means that both supply chains and consumer demand are negatively affected with no certainty of how long this disruption will last and how widespread it will be. The long-term impact on virtually all industries is, as yet, unknown and this too will affect revenues and delay investment decisions.

The growth engine that is China was already slowing down before the outbreak of the coronavirus (COVID-19), which is having a further negative effect. Now that all major manufacturing countries are affected by COVID-19, global growth will be impacted as supply chains are disrupted.

New technologies are being increasingly adopted by the discrete manufacturing industries. These include:

All these technologies have impact beyond manufacturing as it changes the global value chain, bringing production closer to the consumer.

The discrete manufacturing industries are typically impacted faster and more dramatically than process industries as these short cyclical industries cut and increase CapEx faster. Here is a snapshot of how ARC sees capital expenditures developing in some key discrete manufacturing sectors:

More detailed discussions of the above industries follow.

In 2019 the aerospace & defense (A&D) industry began with strong growth, but this has slowed down and Q4 was flat. Global uncertainty about the business cycle, trade wars, the Brexit, and finally the Coronavirus, which impacts travel volumes, are among the reasons. Among the heavyweights, Boeing is facing tough times with the problems around their 737 Max and the recent announcement that subsidies may be cut; on the other hand, WTO allowed tariffs against airbus in the US. Both companies have lowered their CapEx spending.

Defense budgets have been rising continuously for many years and the pressure from the USA on NATO partners is likely to increase spending further. Especially the USA and China are further increasing their budgets.

A&D, a high-technology manufacturing industry, is a leader in innovating and executing both product design and manufacturing engineering. The goods produced by the A&D industry, including commercial and military aircraft, space systems, and ground defense systems, are typically high-value assets and often mission- and/or safety-critical. So, while demand is driven largely by global trends in defense spending and commercial aviation, competition revolves around product innovation and optimization. For example, small gains in aircraft fuel efficiency, via light-weighting, improved aerodynamics, or engine optimization can provide significant cost savings when applied across fleets over their operational lifecycle. Customer willingness to pay a premium for such benefits drives tremendous R&D spending and results in mid- to long-term expansion and contraction cycles that align with the development lifecycle of next-generation products.

Pressure to accelerate development cycles, reduce cost, and increase capacity is generated at the end user level. The ten largest companies account for around two-thirds of the total industry revenue and this percolates down through the expansive A&D supply chain. This pressure is magnified if the supply chain is not elastic enough to respond adequately to the shifts in demand caused by global trends and the business cycle discussed above. When this occurs, we often see significant increases in horizontal consolidation and vertical integration for scale and cost effectiveness.

Overall, commercial aircraft backlog starts to decline from peak levels, while regional jet demand is increasing. Short-term demand for the current generation of commercial aircraft is driven by the need for carriers to replace older airframes. While the economic fundamentals are fine, there are other factors hampering growth and lowering investments and revenues. The Coronavirus has significantly impacted traveling, especially in Asia. This is impacting the revenues of all the airlines; while it is likely to bounce back, the lost revenues will reduce spending. The constant tariff war between USA and Europe continues and is increasing prices for airlines on both sides of the Atlantic. The recent announcement of the US administration to cut subsidies for Boeing may have a larger impact and increases uncertainty. Boeing’s revenue is heavily impacted by the 737 Max issues, as a heavyweight in the industry and our index, this does impact the values on a global scale. With most of these factors being temporary, ARC expects the commercial aircraft sector to stabilize in 2020 and return to a growth pattern in mid-2020.

Defense spending is continuously rising. As the US pulls out of selected conflicts (while continuing to increase their own defense spending) global uncertainty is rising and defense expenditures are increasing. The pressure on NATO partners to increase spending also benefits the industry.

Going from the Atlantic to the Pacific, tensions along the borders in the South China Sea will keep spending high in all involved states. Also, the Korean conflict won’t be resolved. Defense expenditures are increasing in China and its neighboring countries. The situation in the Middle East (Syria, Yemen, Iran, Libya, among others) is not stabilizing and governments continue to invest in their defense budgets.

The long-term outlook looks promising. Rising wealth in Asia is increasing air travel globally; however, in the developed nations one of the factors that will lower air traffic is declining populations, which affects mainly Japan plus selected European countries. The full impact of COVID-19 can be assessed only at a later date.

In the long run, trends, like fuel efficiency, will continue pushing the market towards the most modern manufacturing technologies. Additional trends include electric propulsion aircrafts (in early stage of development), automated flight deck (already quite advanced), and urban air mobility (in early stage of development).

Requirements by commercial aircraft customers will push manufacturers to invest in new production methods and reshape their processes as well as the global value chain. Among the drivers are increasing demands in terms of delivery schedules and customization, traceability of parts, lower fuel consumption, XaaS, or predictive maintenance capabilities.

In the long run defense budgets are expected to continue to rise, also pushing the market. The one-time project character of many defense projects pushes the manufacturers further towards digitalization, which in turn triggers demand for cybersecurity.

Most EBIT measures have increased over the last few years, due in part to increased demand and improvements to established manufacturing lines and supply chain efficiency. This behavior often follows periods of high CapEx, coinciding with the onset and eventual resolution of quality and run-rate issues associated with new production lines, capacity expansions, and supply chain dynamics.

Further, as mentioned earlier, large and mid-sized companies are pursuing acquisitions and mergers aggressively to better manage cost and scalability within their supply chains, increase negotiating leverage, and gain access to new technologies.

The dip in EBIT KPIs in 2019 is solely caused by Boeing.

With light and shadows in 2019, the long run perspective is bright for the aerospace & defense industry. From an automation perspective the increasing demand from airlines and commercial and public customers will continue to push the adoption of the latest technologies, including robotics, PLM, additive manufacturing, or others.

ARC Advisory Group clients can view the complete report at ARC Client Portal

If you would like to buy this report or obtain information about how to become a client, please Contact Us