Representative End User Clients

Representative Automation Clients

Representative Software Clients

Looking back at the early 2000s, four countries drove global growth in industrial markets: Brazil, Russia, India, and China. Annual growth in these countries, known collectively as the “BRICs,” hovered at around 7 percent. This made it relatively easy to plan and forecast with reasonable accuracy.

Now things have changed, with no single country or groups of countries standing out as a driver of global growth. While China and India remain strong, growth in Brazil and Russia has fallen into the low single-digits. Meanwhile, the high-growth countries tend to be small and their markets harder to access. This makes them less appealing for industrial automation suppliers looking to expand into new markets. So where exactly should companies look for growth today?

In this report, we look at specific areas of growth in automation markets over the next five years. In general, these are the countries to keep on your radar. The information presented here, from ARC’s Country Market Analysis Reports, includes the following key findings:

Economic growth is a complex topic that can’t be summed up accurately with a single number. Growth can be deceiving for industrial manufacturers and suppliers looking to expand their businesses. Is it better to invest in a small country with high growth, or a large country with modest growth? If a country is forecasted to have high growth, how much can a company expect to reap if it invests there?

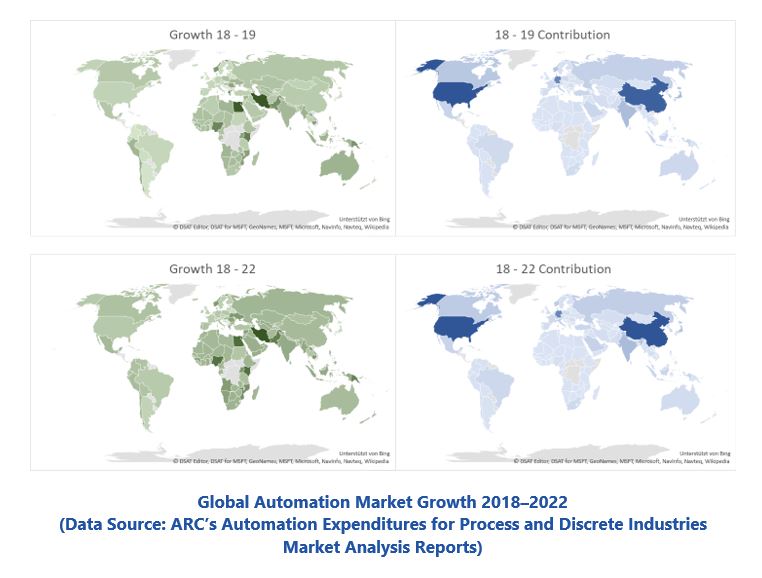

The chart below shows two aspects of GDP growth. The green maps on the left show annual growth – the darker the color, the higher the growth. Countries such as Romania, Norway, Egypt, and Iran expect to enjoy high growth, so their color is dark green. The graphs on the right show a slightly different picture. The blue color depicts growth contribution, which is a combination of market size and growth. The darker the blue, the higher the growth contribution. In this chart, large countries like China, the US, and Germany appear to make the largest contribution to global market growth.

In general, smaller countries with high growth rates will have less of an impact on the overall market growth in any given year than much larger countries with lower growth rates. As an example, consider a global market that expands from $100 to $110 million in one year; while the market growth in a small country in the same year doubles, let’s say it grows from $1 to $2 million. That country’s market grows by 100 percent, but it contributes only 10 percent to the world market’s growth. A large country that grows from 60 to 63 percent of the world market (5 percent growth in the country) contributes 30 percent to worldwide growth. Measuring a country’s growth by its contribution to global growth obviously favors the established giants.

While the left-hand chart on the previous page highlights areas of growth around the world, the right-hand chart makes it clear that automation markets will continue to derive the highest contribution from large, established markets. Since the larger countries, such as Germany and the US, also often host large cluster of OEMs that export to all regions and countries, they also benefit from growth in smaller emerging economies.

Industrial companies that are already well established in the blue markets might want to keep an eye on the green countries in the first chart.

Many of the fastest growing countries in our list are small and have experienced a turbulent past, from which they are expected to recover (Iran, Syria and Ukraine). Growth potential is currently high because these countries are either investing in infrastructure (or rebuilding it), or building new plants or upgrading existing plants. In addition, due to the time window, a second group of commodities-based economies, such as Brunei, Papua, Nigeria, and Norway, show good potential for growth. The third group consists of countries that will likely invest in more automation due to rising wages and increased standards of living. These include Pakistan, Cambodia, Laos, Vietnam, and Angola. These are interesting countries for manufacturers, but investment here can also be risky. It’s likely that Egypt will remain at the current growth level, and current geopolitics prevent a reasonable forecast for Iran.

Countries that ARC believes will experience high growth while maintaining a stable framework are Romania, Chile, India, and Saudi Arabia.

Slow growth countries are often mature, such as Japan, France, Italy, and the US. In these countries, exports cannot make up for lack of internal market growth. In other slow-growth countries, such as North Korea, Belarus, UK, Brazil and Italy, political challenges are likely to hamper growth. In selected countries that have a distinct industry mix, such as South Korea and Japan, the current high level of investment in those industries will limit growth over the next years. Countries such as France and Argentina offer potential growth opportunities in selected sectors but are likely to experience sluggish overall growth.

Some countries may experience structural breaks, due to the political situation. Many of these countries are small, with several notable exceptions: Mexico, Taiwan, South Korea, and the UK. Mexico is affected by arbitrary trade disputes with the US, while South Korea and Taiwan are affected by import substitution measures from China. The UK will likely undergo severe structural changes when it ends its membership in and trade relationship with the European Union in March 2019.

Next, we’ll take “deep dives” into countries that ARC believes will have particularly good growth potential for automation suppliers in the next five years.

The Romanian economy is highly diverse and enjoys a high share of industrial value-add from its extensive industrial base. Since it joined the EU in 2007, government economic measures and communist-era educational excellence have spurred rapid growth. European Union subsidies, low wages, and an inflow of foreign investment also played a large role. A key advantage of Romania is its role as a geographical link between the EU and the East. Located on the Black Sea, Romania also connects the Middle East and Russia to Europe. Bucharest, the capital, is one of the largest financial and industrial centers in Eastern Europe.

Today, the period of double-digit GDP growth has ended, just as the era of automation begins. In recent years, Romania’s economy was among the fastest growing in Europe by GDP. Growth rates were even higher prior to the late 2000s crisis when the local mining and oil sector also drove growth. Starting in 2017, consumer demand growth slowed down, and a slowdown in overall growth followed. However, manufacturing and private investment will continue to drive growth, even if they cannot fully counter the slowdown in private consumption and public investment. Inflation is beginning to rise and, consequently, interest rates started climbing in late 2017.

In 2018 and 2019, Romania will experience increased investment, driven by the general manufacturing uptick and EU subsidies that address infrastructure. Looking forward, there is still room for growth from an increasing market for automation-related services.

India’s government launched its “Make in India” initiative in 2014 to encourage foreign manufacturers to invest in the country. The program, which opened 25 sectors to full foreign investment, drew $240 billion worth of investment commitments. This makes India the world’s most attractive country for foreign investment. Combined with other initiatives, India improved its position in several international indices, including ease of doing business, global competitiveness, and logistics performance.

India imports almost 80 percent of its oil and gas and the industry plays an important role in the country’s economy. The recent slump in global oil prices has benefited the refining sector and helped the country reduce its trade deficit. India has emerged as a refining and petrochemical hub, with exports of refined petroleum products contributing significantly to its high foreign exchange earnings. India has the potential to become self-sufficient in oil and gas someday, as over 55 percent of the 3.14 million square kilometers of the country’s sedimentary basins are either poorly explored or unexplored. India’s government is targeting an investment of $100 billion in the oil & gas sector in the next five years as part of its Make in India plan.

The following facts help illustrate the attractiveness of the Indian oil & gas market for automation suppliers:

Saudi Arabia is a country of great opportunities, but also great challenges. It is oil and capital rich, but it plans to further diversify its industrial base to reduce future dependence on petroleum. Within this framework, industrial companies can expect strong growth potential. However, doing business is not easy and automation markets are difficult to access. Most equipment needed in Saudi Arabia is not purchased locally, but rather as part of complete systems from foreign suppliers. Purchasing decisions for automation systems are often made in faraway countries. Thus, it is important for suppliers to understand how the supply chain works.

Foreign investment licensing in industrial activities is governed by the Saudi Arabian General Investment Authority (SAGIA). With a view to attract more FDI, the regulatory authority is trying to reduce the timeline for obtaining a license by simplifying registration formalities and implementing online systems for payment and documentation. Still, many firms continue to partner with local companies to comply with local policy requirements and manage bureaucratic hurdles. The Saudi government is offering financial incentives like soft loans, export credit, and insurance, to encourage foreign investment. These initiatives keep the country ahead of the overall Middle East North Africa (MENA) region in credit index.

Automation demand will remain solid in the coming years. Because the state-owned Saudi Aramco manages upstream oil segment activities, import of technology, adoption of state-of-the-art automation, and hiring talent are all important for the country to remain globally competitive. However, since foreign investment is banned in the upstream oil sector, it is extremely difficult for foreign automation and process technology suppliers to access this otherwise lucrative market.

Foreign investment and joint ventures (JV) in the downstream sector, specially refining and petrochemical, have been picking up lately. For instance, companies like ExxonMobil and Shell have formed partnerships for downstream refining, bringing leading-edge technologies and innovation into the country. Technology selection usually rests with the foreign JV partner that acts as the gatekeeper and decides on the automation products and solutions to be adopted.

Chile, the world’s leading copper producer, boasts of world-class mining infrastructure and operations. In 2016, the country produced 5.55 million tons of copper, representing 30 percent of current world production. Not surprisingly, the mining sector plays a key role in the economy, accounting for about 10 percent of GDP and about 50 percent of exports. The mining project pipeline remains large, but less certain than in previous years. Projects are under development by both state-owned and private companies, but at a more moderate pace compared to the years when copper prices were historically high. Permitting is onerous and often involves more than a dozen agencies, particularly for large investment projects.

Capital outlay projections in the copper mining sector for the period 2017-2024 are expected to be in the $25–30 billion range. In addition to copper, Chile is also a major supplier of molybdenum, gold, and silver. The country also supplies non-metallic minerals such as iodine, lithium, sodium, and potassium nitrate.

Chile is also the world’s second largest lithium producer, with a 36 percent share of the world market. The country holds the largest known economically extractable reserves of lithium in the salt flat of Salar de Atacama. Increased demand from the electronics and electric vehicle industries has made this resource very attractive to international investors and developers.

With its low-cost labor force, a free-trade agreement, and a 3000+ kilometer border with its rich neighbor to the north, Mexico should be well-positioned to become a high-income country. The North American Free Trade Agreement (NAFTA), signed in 1994, was a gift to Mexico that should have driven up the country’s GDP, bolstered wages, and reduced unemployment. And yet, most of Mexico’s peers in Latin America outperformed the country economically in the quarter century of NAFTA. This disappointing performance has many causes, including competition from China, exposure to volatilities in US financial markets, and the flexibility of Mexico’s exchange rate.

Despite the country’s poor economic performance in the NAFTA years, Mexico remains an attractive location for manufacturing companies that want to make products close to and access the lucrative US market. In 2017, a full 80 percent of Mexico’s exports were shipped across the border to the US. Now that NAFTA has been renegotiated with only minor changes, fears of the unpredictably of Washington’s changing policies have now subsided.

Mexico's manufacturing sector is growing fast and attracting foreign investment. Industries such as automotive, aerospace, consumer electronics, and medical devices offer distinct opportunities to implement cutting-edge automation. Robotics are an important market thanks to their widespread use in local automobile production. Use of robotics will grow as wages increase and factories need to produce to global standards.

For automation suppliers, Mexico presents a mixed bag of opportunities. Bureaucracy and red tape can initially make doing business difficult for international manufacturing companies, even as the presence of foreign companies has internationalized the business climate. But long-term investments in Mexico typically have paid off handsomely and the country is likely to weather the current storm from the north.

ARC Advisory Group clients can view the complete report at ARC Client Portal

If you would like to buy this report or obtain information about how to become a client, please Contact Us