Representative End User Clients

Representative Automation Clients

Representative Software Clients

We are at a turning point in the business cycle. Many of the industries have started to slow down; and many machine builders are already expecting to see negative growth.

ARC Advisory Group looks at different discrete manufacturing industries to identify trends in capital expenditures (CapEx) and their drivers. We calculate our CapEx index using the same rigorous methodology we use for the ARC Automation Index, which is based on publicly available data provided by major companies (end users rather than suppliers in this case).

Capital expenditures (CapEx) are a leading indicator for automation markets. When confidence in vertical industry markets decline, a de-cline in investments often follows.

Past experience shows that it takes around eight to nine years following a financial crisis to experience a global upswing. For example, following the global crisis in 2008, the upswing started in 2017, with 2018 being another strong year and a return to a normal business cycle movement. We are seeing the current political uncertainty and trade tensions (such as the US-China trade war and Brexit) dampening growth and affecting long-run investments.

In addition, the growth engines of the past decade are slowing down. South Africa, Turkey, Brazil, Russia, all show weaker growth, but it is predominantly China, which has an impact on the global economy.

In parallel to the economic downturn, we are also in the process of adopting new technologies in manufacturing. Additive manufacturing is impacting traditional machinery markets, artificial intelligence is on the horizon and has the potential to change manufacturing fundamentally. Also augmented reality and the increased use of advanced robotics are penetrating the plant floor. These new technologies also impact the world outside of manufacturing, partly replacing labor but also changing requirements for workers and operators and changing the global value chains by bringing production closer to the consumers.

The discrete manufacturing industries are typically impacted faster and more dramatically than process industries. These short cyclical industries cut and increase CapEx faster. Here’s a snapshot of how ARC sees capital expenditures developing in some key discrete manufacturing sectors:

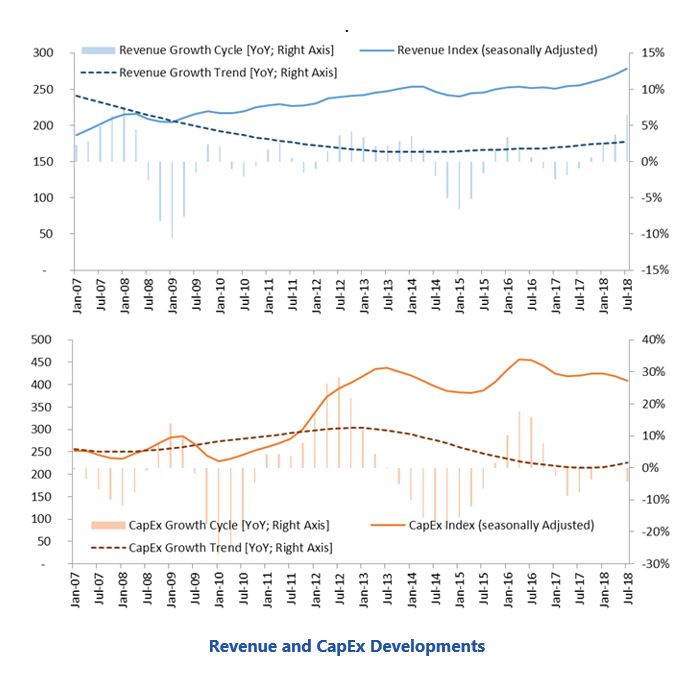

In 2018, the aerospace & defense (A&D) industry experienced a strong rebound in terms of revenue growth and one of its best years of the past decade. This recovery aligns with the historic industry business cycle and, over the next few years, is likely to be reinforced by an increase in both commercial airline and defense spending globally.

A&D, a high-technology manufacturing industry, is a leader in innovating and executing both product design and manufacturing engineering. The goods produced by the A&D industry, including commercial and military aircraft, space systems, and ground defense systems, are typically high-value assets and often mission- and/or safety-critical. So, while demand is driven largely by global trends in defense spending and commercial aviation, competition revolves around product innovation and optimization. For example, small gains in aircraft fuel efficiency, via light-weighting, improved aerodynamics, or engine optimization can provide significant cost savings when applied across fleets over their operational lifecycle. Customer willingness to pay a premium for such benefits drives tremendous R&D spending and results in mid- to long-term expansion and contraction cycles that align with the development lifecycle of next-generation products.

Pressure to accelerate development cycles, reduce cost, and increase capacity is generated at the OEM level. The ten largest OEMs account for around two-thirds of the total industry revenue and this percolates down through the expansive A&D supply chain. This pressure is magnified if the supply chain is not elastic enough to respond adequately to the shifts in demand caused by global trends and the business cycle discussed above. When this occurs, we often see significant increases in horizontal consolidation and vertical integration for scale and cost effectiveness.

The commercial aircraft order backlog remains at an all-time peak. Short-term demand for the current generation of commercial aircraft is driven by the need for carriers to replace older airframes. Likewise, defense spending has seen a significant uptick over the past year driven by geopolitical uncertainty. For instance, China, France, India, and the US have each substantially increased their defense budgets.

In the short term, these trends force OEMs to expand the capacity of their established production lines and search for new technologies and methods to relieve the stress on their supply chains

The short-term demand for commercial aircraft is bolstered by the rap-idly growing aviation markets in China and India where new wealth creation and shifting demographics is leading to increased air travel. This appears to be a steady trend that will be essential to support long-term market growth. In the more established markets of the US and Europe, long-term growth in commercial aviation will be driven by the next generation of lightweight, highly fuel-efficient aircraft. These new products, which rely on high-tech materials and novel manufacturing processes such as additive manufacturing, will dictate capital investment throughout the supply chain.

The long-term outlook for defense spending is also positive. Tension between the US and its long-time allies has forced many European countries to reconsider their reliance on US military presence and will likely induce greater defense spending regardless of future US policies. Furthermore, there is no indication that the growth of defense spending in Asian and Middle-east markets will slow significantly.

Most EBIT measures have increased over the last few years, due in part to increased demand and improvements to established manufacturing lines and supply chain efficiency. This behavior often follows periods of high CapEx, coinciding with the onset and eventual resolution of quality and run-rate issues associated with new production lines, capacity expansions, and supply chain dynamics. At the same time, CapEx stagnated from 2014 to 2018. However, most major OEMs are forecasting increased capital spending over the next three years.

Furthermore, as mentioned earlier, large and mid-sized companies are pursuing acquisitions and mergers aggressively to better manage cost and scalability within their supply chains, increase negotiating leverage, and gain access to new technologies.

The A&D industry is poised to experience strong growth in 2019 and greater CapEx spending over the five-year forecast period. The heavy reliance on cutting-edge technology make it a suitable bellwether of the success of emerging technologies. For example, additive manufacturing, while often too expensive for applications in other industries, can provide operational efficiency benefits that far outweigh associated costs. However, the reliance on cutting-edge technology combined with long development cycles poses significant risk for A&D companies, a risk that must be managed through effective and comprehensive R&D programs.

The A&D industry is also among the hardest hit by the aging work-force, especially in the US. This issue could escalate over the next decade. OEMs and tier 1 suppliers are investigating and investing heavily in automation and IoT-based solutions. This includes augmented reality to curb the adverse effects to operational efficiency and reduce the burden on new employees that accompany workforce turnover.

Revenues in the automotive industry rose moderately on a global scale, while CapEx again recorded good growth in 2018. ARC believes that this is a good indicator for the coming years. CapEx investments in the automotive industry have been at a high level for several years.

The still fast-growing global demand for electric vehicles (EVs) and in-creasing need for mobility, especially in the so-called developing and emerging countries, are important growth drivers for the automotive and related industries; e.g. mining and electronics. However, even the automotive industry was hit hard by the dramatic decline in demand for diesel engines, especially in the EU and US.

Millennial purchasers will drive the future automotive market and, increasingly, the trend appears to be moving away from individual car ownership, mainly in developed countries. Additionally, demographic trends indicate that large urban centers will become denser, where transportation needs will be based on upgraded urban transit systems and electric cars due to the smog issues in big cities.

Already on a high level, after minor growth in 2017, CapEx investments picked up pace again in 2018. ARC believes that CapEx will continue to stay on a high level, but with a slower growth rate in the coming years. Revenues of automotive companies have increased steadily from 2016 to 2018, pushed by the good overall economic climate.

ARC expects 2019 to be challenging for the automotive market, with many uncertainties and thus lower growth than in 2018; revenues will be almost flat with minor growth in CapEx. Over the forecast period, we expect CapEx and revenue to continue to grow, but less so than in previous years.

In 2018, global vehicle sales were challenged, especially by a dropping demand in China and global passenger vehicle sales limping to a marginal increase; currently estimated at around 400,000 units more in 2018 com-pared to 2017.

Automotive manufacturers and suppliers alike face increasing pressure from even tighter networking along the automotive value chain, the on-going electrification of vehicles, entrance of new competitors, high costs, new materials, and penetration of information technologies in production and in the vehicle itself. Demographic, environmental, social, and political developments add additional pressure.

The European auto industry still struggles with ramifications of the UK’s planned exit from the EU (Brexit), plus the ongoing, not totally resolved, consequences of “Diesel Gate” and other scandals. The most significant current downward macroeconomic driver globally, however, is the slowdown of economic growth and continuing trade conflicts be-tween China and the US.

Overall, the EBIT/Revenue KPI remained nearly stable over the last years. This is also true for the output-per-asset ratio, which has remained quite constant in the last period. Even the investment activities were stable on a high level. Looking at the history, CapEx/revenues basically oscillated at around 7 to 8 percent over the last five years.

We’ll continue to see innovations coming from the automotive industry. These will include more use of innovative new technologies such as digital twin simulations of both the production lines and the finished automobiles to further streamline and reduce bottlenecks in production and support continuous product improvements and customer satisfaction. We’ll also see accelerated use of machine learning and other artificial intelligence; robots, cobots, and AGVs; and new advanced algorithms and sensors for autonomous and semi-autonomous vehicles.

ARC believes that these and other innovations will maintain capital expenditures at a relatively high level.

As mentioned, other forces are also at play. All-electric models will gradually supersede the current fleet of hybrid and conventional diesel and gasoline vehicles. Newer designs are making increased use of aluminum, plus new materials like ultra-high-tensile steel and carbon fiber composite to provide the light weight and stronger structure needed for the next generation of vehicles (electric, hybrid, and combustion engine-powered alike). Looking ahead, today’s smarter, more connected cars will soon become fully digitalized, with commercial-scale, fully autonomous vehicles somewhere on the not-too-distant horizon.

A complete business cycle in the global electronics industry typically lasts from five to seven years. After two booming years in 2017 and 2018, the growth rate has slowed in 2019; a trend ARC estimates will last for several years.

Compared with North America and Europe, Asia today is the main manufacturing center of the global electronics industry. Here, China is the biggest country with nearly 35~40 percent of global production capacity. Korea and Japan are also important manufacturing centers. In recent years, Vietnam attracted more investment from multinational electronics manufacturers and developed very fast, largely due to the production capacity shifting from China due to rising labor costs.

The electronics industry is one of the main industries to apply discrete automation solutions. These include sensors, machine vision, PLC, GMC, AC drives, industrial robotics, and MES software. The industry is also developing very quickly due to continuous adoption of new technologies. Increased sensitivity to manufacturing costs drives the need for advanced automation and quality control solutions.

We expect the global electronics market to continue to contract in 2019. It’s likely to recover in 2020, when 5G wireless telecommunication technology will begin to be widely applied, since this will drive the market development of smartphones and system equipment. Our forecast expects that revenue and CapEx will continue to have slow growth rates over the next five years.

We expect that CapEx will continue at a moderate level, due to the quick updating of technologies in the electronics industry and rising labor costs in China. More electronics manufacturers are making new investments in emerging Asian countries, Vietnam in particular. This will help stabilize CapEx spending.

We also expect an ongoing shift towards contract manufacturing, with more electronics companies becoming fabless “brand owners.” Significantly, many of these contract manufacturers are making big efforts to automate their production, especially by using robotics to replace the cost-intensive work force.

Most EBIT measures have increased over the last years. This demonstrates the increasing productivity of the global electronics industry. Looking at the long run, CapEx/revenues are basically constant since 2015 at a long-run trend of around 5 percent.

Today’s global electronics industry faces challenges such as cost, flexible manufacturing, faster delivery requirements, green manufacturing and others.

The main players in the electronics industry also need to adopt the newest technology to differentiate themselves from competitors. All these factors drive the application of automation in this industry. A good example is the Apple iPhone. Every one or two years, the introducing of a new model of iPhone will drive the manufacturing process, equipment, and automation solutions of suppliers in the iPhone supply chains.

ARC Advisory Group clients can view the complete report at ARC Client Portal

If you would like to buy this report or obtain information about how to become a client, please Contact Us