Representative End User Clients

Representative Automation Clients

Representative Software Clients

Automation suppliers continue to see robust revenue growth, posting overall gains of nearly 10 percent versus the second quarter of 2017. Acquisitions and favorable currency exchange rates played a significant role in the revenue growth of many suppliers, but many majors reported strong organic growth during the quarter. The discrete automation sector added considerably to gains, seeing healthy activity in the electronics and automotive industries. After a period of doldrums in the wake of depressed oil prices, the oil & gas sector and other major process industries are seeing more investment activity. Order activity also remained strong, ensuring solid revenue growth in quarters to come.

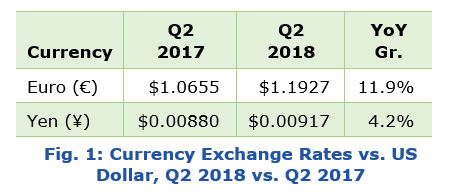

Compared to the second quarter of 2017, the total combined revenues of automation suppliers to both the process and discrete manufacturing industries grew by 9.7 percent (see Figure 2). Process industry suppliers saw their combined revenues grow by 9.7 percent; while suppliers to  the discrete industries saw a 9.1 percent increase in combined revenues. GE Power, due to its large size but relatively small automation component, has an outsized effect on the overall market, so we have removed it from the over-all analysis, though we will continue to cover it in the writeup that follows.

the discrete industries saw a 9.1 percent increase in combined revenues. GE Power, due to its large size but relatively small automation component, has an outsized effect on the overall market, so we have removed it from the over-all analysis, though we will continue to cover it in the writeup that follows.

Among suppliers that report order intake, many saw large increases in activity during the quarter. On average, orders grew by 9.6 percent during the quarter (Figure 3). As with revenues, we have excluded GE from our analysis, which saw a nearly 30 percent drop in orders.

ARC Advisory Group clients can view the complete report at ARC Main Client Portal or at ARC Office 365 Client Portal

If you would like to buy this report or obtain information about how to become a client, please Contact Us

Keywords: Automation Suppliers, Quarterly Results, Asia-Pacific, Europe, Middle East & Africa, Latin America, North America, ARC Advisory Group.